YASKAWA Electric (TSE:6506) reported Q1 FY2027 results on July 10 that, on the surface, look like a miss. Revenue grew 10.6% to ¥139.0bn, while operating profit fell 19.2% to ¥8.49bn — a margin of 6.1%, far below the double-digit levels investors expect from a global automation leader. The stock has corrected accordingly.

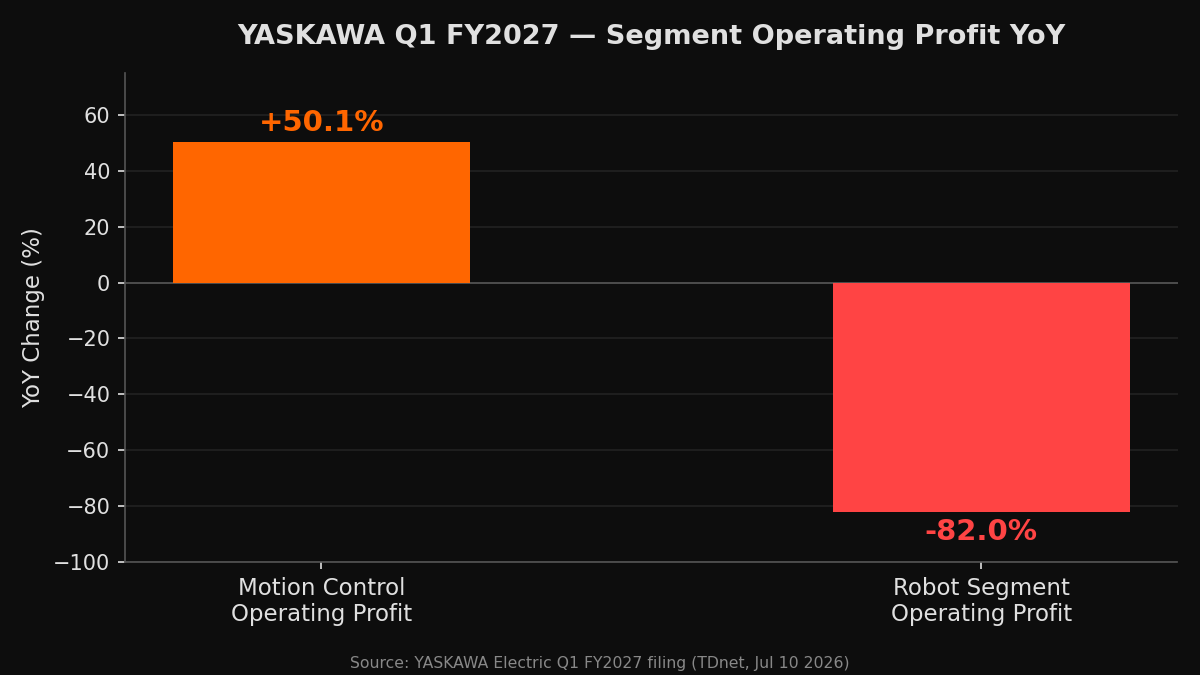

The headline is misleading. Strip away two one-time drags — an ERP system migration that disrupted production lines and European business restructuring charges — and what remains is a Motion Control segment growing operating profit at 50%. That segment makes the servo motors and inverters that sit inside the world’s most sophisticated semiconductor manufacturing equipment. ASML, Applied Materials, Tokyo Electron: they all depend on YASKAWA components that cannot, in practice, be substituted.

The Q1 report is not a business story. It is a clean-up story. The EV robot dream that inflated expectations for two years is over, and the real business — irreplaceable precision motion control for AI infrastructure — has never been structurally stronger.

The Two Businesses Inside YASKAWA

YASKAWA runs two materially different operations that happen to share a balance sheet.

Motion Control makes servo motors, inverters, and machine controllers — the precision actuation systems that move semiconductor wafers, laser cutting heads, and industrial machinery with micron-level accuracy. In Q1 FY2027, this segment posted revenue of ¥67.6bn (+21.5% YoY) and operating profit of ¥7.56bn (+50.1% YoY). Demand is driven by global semiconductor capex cycles, AI data center buildouts, and factory automation across virtually every industry.

Robotics makes industrial robot arms — the welding, painting, and assembly systems deployed on automotive and electronics production lines. In Q1, robot segment operating profit collapsed by 82% YoY. This is the business that has been selling into European EV factory buildouts and Chinese automotive lines — two markets that are now contracting sharply.

The distinction matters because the investment thesis for each is fundamentally different. Motion Control is an infrastructure business with high switching costs. Robotics is a capex-driven industrial business that fluctuates with factory investment cycles.

Why the Robot Business Collapsed — and Why It Was Predictable

The European robot business was built, in large part, on EV factory construction. Volkswagen, BMW, and Stellantis were ordering automation equipment for dedicated EV assembly lines. In December 2025, the EU formally scrapped its 2035 internal combustion engine ban, replacing it with a softer 90% emissions reduction target. The policy reversal was immediate and decisive: automakers froze EV-specific capital expenditure. New EV lines that were planned were cancelled. Orders that had been expected did not arrive. YASKAWA booked restructuring charges as it right-sized its European operation for a smaller market.

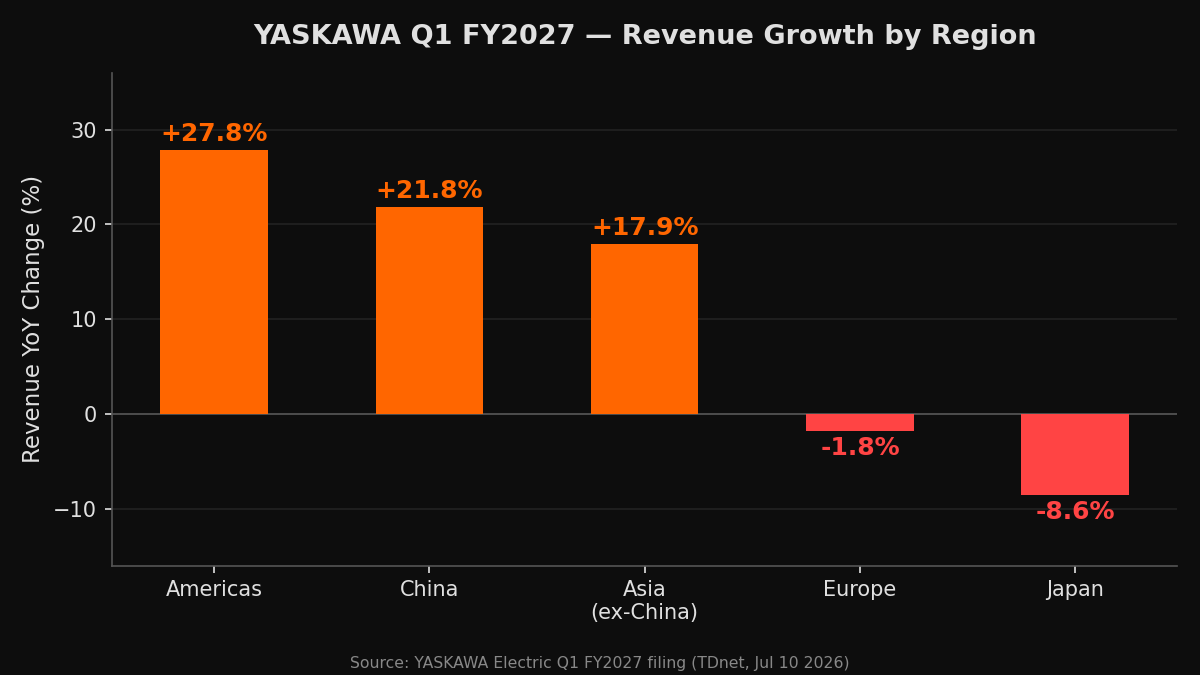

China tells a parallel story with a different mechanism. Chinese EV manufacturers — including BYD — appear to be growing by volume, but the economics are breaking. BYD’s Q1 2026 net profit fell 55% year-over-year. Industry-wide, an estimated 70% of Chinese EV sales are loss-making. Factories are running at below 50% of capacity against a production base of 55.5 million vehicles annually, while domestic sales sit near 23 million. Companies losing money on every car sold do not invest in new automation equipment. YASKAWA’s China revenue grew 21.8% in Q1 — but that growth is coming from semiconductor and AI-linked demand, not from EV manufacturers who cannot fund capex.

The robot business will recover when automotive factory investment resumes at scale. That timeline is tied to EV policy clarity in Europe and financial stabilization in China’s auto sector — neither of which is imminent.

The Moat That Doesn’t Depend on Any of This

The Motion Control segment operates on a different logic entirely.

Servo motors and inverters for semiconductor manufacturing equipment are specified by equipment makers — ASML, Tokyo Electron, Applied Materials — into the design of tools that cost tens to hundreds of millions of dollars each. Once a servo motor from a specific vendor is qualified into a tool design, replacing it requires re-engineering and re-validating the entire system. The switching cost is enormous. YASKAWA, alongside Mitsubishi Electric and Fanuc, occupies this space. Chinese alternatives are not qualified and will not be for years, if ever, in high-precision applications.

This means YASKAWA’s Motion Control revenue grows structurally with global semiconductor investment — a multi-year cycle that is being driven by AI compute demand, advanced packaging, and the geopolitical imperative to build domestic chip capacity in the US, Japan, and Europe. NVIDIA’s partnership announcement with YASKAWA for its Motoman NEXT platform — which runs an embedded Jetson Orin processor — signals the next phase: AI-native robot systems that extend the Motion Control franchise into the physical AI era.

Valuation and What Comes Next

At 5,445 yen (July 15 close), YASKAWA trades at approximately 30x earnings on current depressed Q1 results. Analyst consensus targets average 6,859 yen — roughly 26% above current levels — with 11 of 17 analysts at buy or strong buy.

The full-year guidance — revenue ¥580bn (+7%), operating profit ¥60bn (+26.8%) — implies a sharp profit recovery through Q2-Q4. With ¥8.49bn earned in Q1, YASKAWA needs ¥51.5bn across the remaining three quarters, or approximately ¥17bn per quarter. That is an aggressive ramp from a weak starting point.

The Q2 results (due October 2026) will be the first real test. If ERP migration costs are genuinely one-time and European restructuring charges do not recur, the underlying Motion Control momentum should begin to show through. If Q2 is also weak, guidance credibility will be questioned.

For long-term holders, the thesis does not depend on Q2 execution. There is no credible alternative to YASKAWA’s Motion Control components in semiconductor equipment. As long as the world continues building AI infrastructure — which it will, at scale, for years — YASKAWA’s core business grows. The current valuation reflects a noise event. The structural story is intact.

Figure 1: Q1 FY2027 — Motion Control operating profit +50% vs Robot segment -82%

Figure 1: Q1 FY2027 — Motion Control operating profit +50% vs Robot segment -82%

Figure 2: Revenue growth by region — China and Americas lead, Europe and Japan drag

Figure 2: Revenue growth by region — China and Americas lead, Europe and Japan drag

Source: Original filing (TDnet) | 日本語版

Disclaimer | This article is for informational purposes only and does not constitute investment advice.